Weekly Brickser' feed

Big players back in the game? and spotlight on a Lisbon opportunity

Hello Readers!

Recent years have witnessed profound social, cultural, and economic shifts, reshaping our engagement with and investment in real estate. Join me in navigating the complexities of the property market, as we decode the nuances behind the ever-changing world of bricks.

A Tale of Economic Stability

The US economy has demonstrated remarkable resilience, buoyed by high confidence levels and employment figures that, so far, have shown no signs of faltering. As a European with a penchant for critically examining the US model, I've often braced for a tumultuous recovery period. Prepared for a scenario of prolonged high inflation and brittle consumer spending, I, unlike many of my US counterparts, take a certain pride in my ability to not only pinpoint Brazil on a map but also to toggle off my critical lens when necessary. It seems we're amidst a significant resurgence in the global economy—a phenomenon often spearheaded by the United States.

While the global economic landscape remains at the mercy of geopolitical shifts, especially in Eastern regions, the overall trend is undeniably positive. This wave of cautious optimism is even beginning to wash over Europe. As we transition from the end of 2023 into early 2024, Eurozone inflation, which once soared to a peak of 9.2%, has now softened to around 3%. This marks a considerable easing, heralding a moment of economic recalibration.

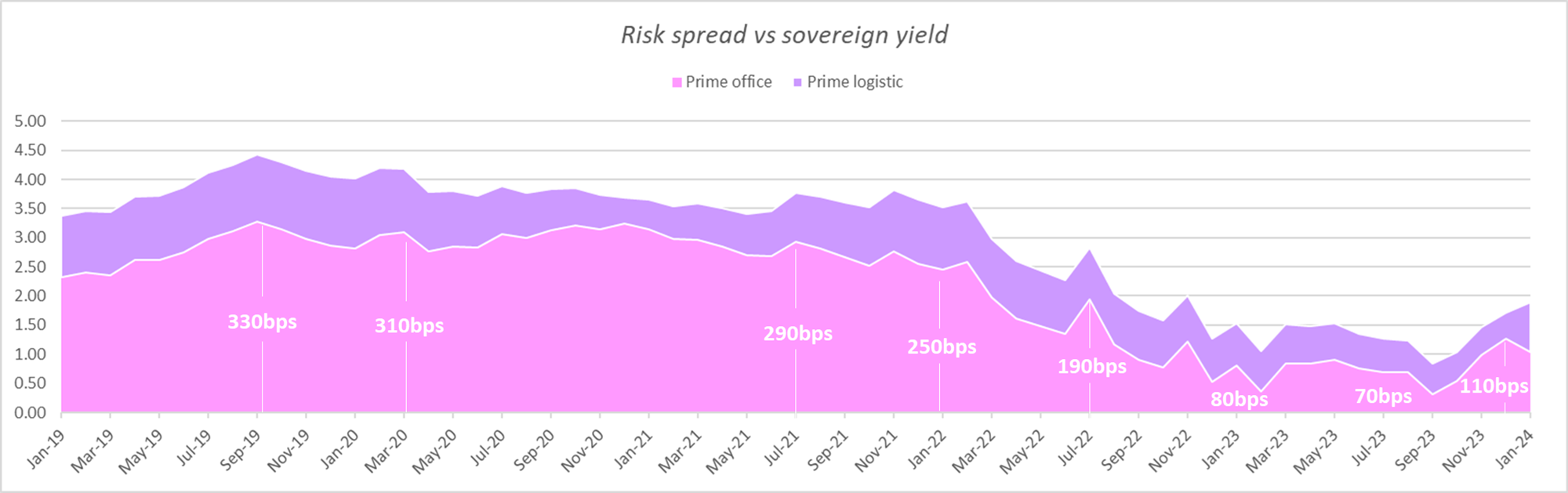

.png")

The recent easing of sovereign yield levels is a tangible sign of the broader economic shifts underway. Currently, the yield on the French OAT TEC 10 is around 2.8%, marking a significant decrease from its October 2023 high of 3.5%. The 10-year German Bund yield has similarly reduced to approximately 2.2%, moving away from its September peak of 3%. Across Europe, the trend in average yields on sovereign bonds, echoing levels not seen since the end of 2022, signals a period of stabilization and growing optimism.

However, the return to yield levels last observed in 2012-2013 serves as a poignant reminder of the need for careful economic recalibration. This situation, where improvement and caution must coexist, underscores the need for strategic adjustments in response to these historically significant yield trends. We must resist complacency; the changes we face demand a shift in our lexicon beyond the euphemistic term “adjustment.”

“Adjustments” in Prices

In keeping with these new standards, the past three months have seen a flurry of announcements from fund managers regarding adjustments in portfolio valuations. Just a few days ago, Keppel Pacific Oak US REIT reported a 6.8% year-on-year decrease, following similar revelations from Cromwell, Elite Commercial, and others.

This trend might appear as a gentle reassurance to limited partners (LPs) and private investors, a marketing strategy to cushion the blow. The proclaimed alignment with the new reality suggests that investor savings are largely safeguarded. Yet, the reality on the ground paints a different picture: a significant yield decompression has already taken place, with asset valuations plummeting by 10% to 40% for those considered liquid. This adjustment, far from being a mere recalibration, indicates a profound shift in market dynamics.

Indeed, while prime assets have shown resilience, undergoing only limited adjustments, the landscape of the real estate market reveals nuanced shifts. The risk premium for prime European office spaces has indeed risen, yet it remains at approximately 110 basis points—merely half of its historical average. This subtle increase hints at a relatively stable valuation within the prime sector. However, venturing even slightly beyond the prime assets and categories exposes a starkly different reality. As the market diverges from these prime premises, the adjustments become more pronounced, unveiling a window of opportunity. This divergence suggests that, away from the prime sector's relative safety, there lies potential for significant investment gains for those willing to navigate the complexities of the broader real estate market.

Large buyers redirecting their allocation toward RE

In a notable shift last year, Blackstone significantly reduced its real estate investments, dropping from $47 billion to just $9 billion in the first three quarters. Intriguingly, a considerable portion of its property investments was directed towards the European market. Looking ahead to 2024, Blackstone is poised to concentrate the $40 billion in "dry powder" it has amassed primarily on European properties. This strategic pivot suggests that major investors are recognizing a pivotal moment in the European real estate market, perhaps anticipating that the market is nearing its bottom. This movement is not isolated to Blackstone alone; other institutional investors are similarly expanding their real estate portfolios.

Blackstone official: “the firm has $40bn of “dry powder” — funds raised but not yet invested — and is targeting its investment in parts of the real estate market”

A closer examination of Blackstone's investment direction underscores a targeted approach towards significant industrial deals, residential developments, and data centers. Guess who’s missing? By eschewing the traditional allure of commercial office spaces, these key players are adapting to the evolving market dynamics, prioritizing sectors that promise higher resilience and growth potential in the face of changing work patterns and economic conditions. This strategic realignment suggests a recalibration of investment priorities, aiming to align with the anticipated demands of tomorrow's real estate market.

What does this tell us?

The whales are silently navigating through the currents steering towards the next wave of capital appreciation. In their voyage across the geopolitical tempests, they've charted a course that, for the time being, deliberately bypasses the harbors of office real estate. This strategic shift warrants our close attention. We should observe and possibly follow their lead with discernment. We are navigating not just through numbers, but through evolving trends and momentum. The course they set, subtly avoiding certain waters, invites us to read between the lines, to understand the undercurrents that are shaping the future landscape of real estate investment.

A closer look at Bricks.co Portuguese deal

In today's spotlight, we delve into the fundraising landscape, focusing on an intriguing proposition from the French property fractional specialist, Brick.co. Those familiar with my views know I've been a vocal critic of the company. My skepticism was particularly piqued by their Series B fundraising, which I labeled a speculative venture at best, given it hinged on an undefined valuation. Their approach seemed all sizzle and no steak: a portfolio promising unrealistic yields, lacking robust management, with the celebrity endorsement of Tony Parker serving as little more than a decorative garnish.

However, recent developments compel a reassessment. Brick.co's latest executive appointments appear to mark a significant pivot, bolstering their management team and, potentially, their operational capabilities. This evolution warrants attention, prompting a more nuanced view of their portfolio and deal-making strategies. As always, vigilance is key. We'll continue to track their progress closely, offering updates on whether these changes signal a genuine turnaround or merely a new chapter in an ongoing saga.

The apartment, located in the sought-after Lapa - Estrela neighborhood and part of a historic building, spans 173 sqm. The renovation plan aims to quickly refurbish the apartment, preserving period features while incorporating modern enhancements, with a budget of €200,330. Expected to attract families or buyers seeking a prime residence, the project forecasts a profit margin of 22.7% of the total project cost, with ARIYA Portugal PDP SASU.

Strategy : 6/10

The current momentum in the high-end residential market suggests potential for underpriced opportunities across Europe. However, success in this niche hinges critically on timing and management, given its inherently limited scope (few streets) and select clientele. Here, Brick.co's venture appears to lean more towards an upper-class segment rather than true luxury, raising questions about the target market's availability in Portugal within a desirable timeframe. Plus, is Lisbon the best location to start a strategy like this one? I doubt it.

Location : 8/10

For once, they have done a good job sourcing a very well located asset in the city center of Lisbon. Nice street profiting from an outstanding architecture corresponding to high standard customers. Still some reservations about the relevancy of Portugal for a luxury play at this stage of the cycle.

Manager: 3/10

And here we hit a wall—Who's steering this ship? Nothing about the manager whereas how pivotal his role is for such a play... Sure, they're throwing in 9% of the total cost, a scant but existing consolation.

Overall play : 5/10

A prime location is a good start but not enough to make a good deal. The lack of clarity on management and the asset's questionable market positioning raise doubts about achieving a successful exit.

Plus, why park my fund in a 20% margin refurbishment play in Portugal when comparable or better liquidity and returns might be available elsewhere? Why should I will only be paid 9% for a bond backed by a ghost manager (or worse by Bricks.co itself) when I can get similar cash flow with corporate bonds or prime regional office plays?

Also, when it comes to fractional Real Estate, the whole point must be to democratize access to institutional-quality deals (professional management, risk diversification, etc.). This single-unit adventure, burdened with hefty fees for what exactly? It could be, should be, maybe must be a solo flight or a small crew venture without Bricks.co taxing the journey.

While I will not be participating in this deal, it's not the least appealing proposition I've encountered on this platform. I remain open to exploring future opportunities that present a more compelling case.

Readers, your insights, challenges to the viewpoints shared, or suggestions for future discussions are more than welcome. Please don't hesitate to reach out!

See you next week!

Thank you for your vision